What is the difference between cost control and cost management?

Cost management and cost control are two terms that often get mixed up. If you think about the words, what sounds better?

Would you rather be in control or managing your costs?

It turns out that cost management and cost control really are two different things, and yet they are equally important to have in place!

In this article we look at the difference and how they relate.

Cost Management

Cost management is concerned with the process of planning and controlling the budget of a project or business. It includes activities such as planning, estimating, budgeting, financing, funding, managing, and controlling costs so that the project can be completed within the approved budget.

Cost managementcovers the full life cycle of a project from the initial planning phase towards measuring the actual cost performance and project completion.

Cost management is a continuous process that takes place during the project to determine and control the resources needed to perform activities or create assets:

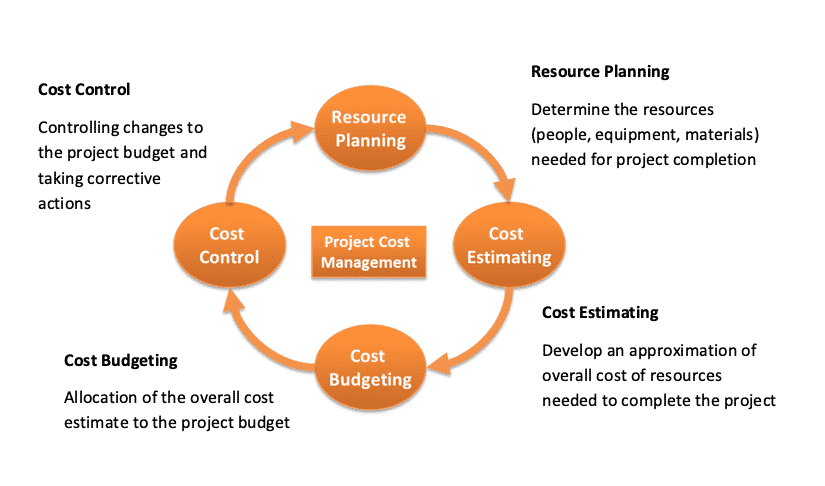

Cost Management Process

Resource Planning

In the initial phase of a project, the required resources to complete the project activities need to be defined.Work Breakdown Structures (WBS)and historical information of comparable projects can be used to define which physical resources are needed. You can think of the required time, material, labor, equipment, etc. Once the resource types and quantities are known the associated costs can be determined.

Cost Estimating

Several cost estimating methods can be applied to predict how much it will cost to perform the project activities.

The choice for the cost estimation techniquesdepends on the level of information available. Analogous estimating using the actual cost of previous, similar projects can serve as a basis for estimating the current project. Another option is to use parametric models in which the project characteristics are mathematically represented. Estimates can be refined when more information becomes available during the course of a project. Eventually, this results in a detailed unit cost estimate with a range of accuracy. Remaining uncertainties in estimates that will likely result in additional cost can be covered by reserving cost (e.g. usingescalationandcontingencies).

Cost Budgeting

The cost estimate together with a project schedule forms the input for cost budgeting. The budget gives an overview of the periodic and total costs of the project.

The cost estimate defines the cost of each work package or activity, whereas the budget allocates the costs over the time period when the cost will be incurred.

A cost baseline is an approved time-phased budget that is used as a starting point to measure actual performance progress.

Cost Control

Cost Control is concerned with measuring variances from the cost baseline and taking effective corrective action to achieve minimum cost overruns.

Procedures are applied to monitor expenditures and performance against the progress of a project. All changes to the cost baseline need to be recorded and the expected final total costs are continuously forecasted.

When actual cost information becomes available, an important part of cost control is to explain what is causing the variance from the cost baseline. Based on this analysis, corrective action might be required to avoid cost overruns. Tight cost control gives a company considerable influence over its cash flows and reported profits.

As a cost controller, you have to actively expedite the scope of work and analyze its progress. Basically, you continuously have to be aware of these elements:

Know what has to be done: you usea detailed budget estimate and tracking profiles, which provide cost control and scheduling bases. This is based on the information from the previous cost management steps: you rely on them for an accurate budget and detailed activities of which the performance can be measured.

Know what has been done: you setup reports providing actual performance data that is consistent with the detailed budget, in a timely fashion.

Know how actual performance compares with performance norms:makeanalyses of the performance to date. The quality of this comparison is only as good as the input you are receiving as controller: the resolution and accuracy of the baseline and the timeliness and correctness of progress reports.

Know what remains to be done:forecast the potential result of the current situation, in case no action is taken to the current performance.

Identify and implement corrective actions:providecontrol in order to bring the project’s performance in line with the expectations. The output of this is an adjustment of the baseline plan: the resources, estimate, schedule, budget, etc. have to be adjusted and the cost management circle continues.

Check results of corrective actions:verify if the goals of corrective actions were achieved. See if you really are in control.

Thus, while cost control seems to ‘limit’ itself to controlling the project during execution, the effectiveness of it is determined by how well cost management processes are implemented and connected. If our people work on each step of cost management separately, without alignment and sharing of information, you might be ‘controlling’ your project, but you are not doing cost management.

Starting a project with cost management in mind will help you avoid certain pitfalls that may occur otherwise.

If expectations of the project are not clearly defined at first, or are changed during the course of the project, cost overruns will be more likely. If costs are not fully researched before the project, they may be underestimated, which might give false indications about the project’s success.

A dollar gained in revenue is a very good thing, but remember: only a small portion in the end reaches the earnings. A dollar saved from cost, however, goes directly to the bottom line. Focusing on understanding and managing costs is a path to ensuring long-term value creation.

Elmer Sachteleben is an experienced certified cost engineer (CCE) and a frequent speaker at industry events. Elmer holds an MSC in applied physics. After providing consultancy services to major companies using the project controls softwareCleopatra Enterprise, Elmer now leads Cost Engineering Academy.

He applies his broad experience and enthusiasm to provide traineeships, develop courses and organize workshops in the field of project controls and turnarounds. He is also a teacher at the Dutch Association of Cost Engineers (DACE).

Elmer has provided consulting services and in process assessment, development, and implementation to major multinational companies such as Shell, Unilever, Bayer, Cargill, CB&I, Mott MacDonald, Heineken, Vopak, Enbridge, Yara, and Rijkswaterstaat.

![[Free 90-min Masterclass] The Ultimate Leadership Recipe for Project Professionals](https://www.projectcontrolacademy.com/wp-content/uploads/2024/08/4-2048x1152.jpg.webp)